On 26 February 2025, the Economics Research Center of the University of Cyprus presented its proposal for an upcoming tax reform. This initiative aims to modernize Cyprus’s tax system while ensuring alignment with European standards. The proposed changes are currently under review by the Ministry of Finance before submission to the Council of Ministers and, subsequently, the House of Representatives for approval. A public consultation period is also expected before the finalization of the reforms.

These changes are still in the proposal stage and subject to further amendments. Some provisions may take effect in 2025, while full implementation is anticipated in 2026.

Key Proposed Changes

Personal Income Tax

- Increase in Tax-Free Allowance: The tax-free annual income threshold is proposed to increase from €19,500 to €20,500.

- Adjusted Tax Brackets: Revised tax rates and income bands are proposed as follows:

| Taxable Income (€) | Tax Rate (%) |

|---|---|

| Up to 20,500 | 0% |

| 20,501 – 30,000 | 20% |

| 30,001 – 40,000 | 25% |

| 40,001 – 80,000 | 30% |

| Over 80,001 | 35% |

- New Deductions for Families and Individuals:

- Additional tax-free allowance for parents with children.

- Deductions for individuals with housing loans for primary residences or rent payments.

- Tax relief for green home upgrades.

Corporate Income Tax

- Increase in Corporate Tax Rate: Corporate tax is set to rise from 12.5% to 15%.

- Abolition of Deemed Dividend Distribution Rules: A significant simplification benefiting corporate structures.

Special Defence Contribution (SDC) Adjustments

- SDC on dividends for Cyprus-domiciled and tax-resident individuals will be reduced from 17% to 5%.

- The SDC on rental income will be abolished.

Stamp Duty and Other Adjustments

- Stamp Duty Limitations: Stamp duty will only apply to agreements concerning real estate transactions, banking, and insurance contracts.

- Extended Tax Loss Carryforward: The tax loss carryforward period will be extended from 5 years to 10 years, subject to specific conditions.

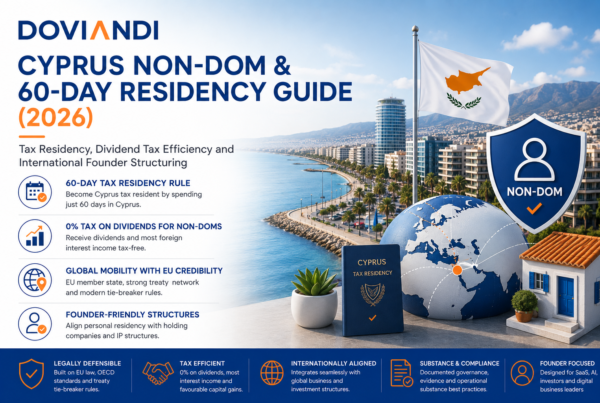

- Tax Residency Criteria for Individuals:

- The 60-day tax residency rule will remain in place.

- Individuals with business ties in Cyprus may also qualify under the revised residency criteria.

- New Treatment of Ex-Gratia Payments & Stock Options:

- Ex-gratia payments will be taxable for employees (subject to capped tax-free allowances), while employers may claim deductions.

- Stock options, under certain conditions, may be taxed at a reduced rate at the time of exercise.

Green & Digital Investment Incentives

- Tax incentives for green and digital transformations:

- Eligible expenses for sustainability and digital transition may qualify for super deductions or accelerated depreciation.

- There will be no restriction on carrying forward tax losses from such expenses.

What Stays the Same?

Despite these proposed changes, Cyprus will retain its competitive tax advantages, including:

- Non-Domiciled Tax Status for foreign nationals relocating to Cyprus.

- Notional Interest Deduction (NID) on new equity.

- Intellectual Property (IP) Box Regime, offering significant tax advantages.

- Tonnage Tax Regime for shipping companies.

- 50% income tax exemption for first-time employees in Cyprus.

What This Means for Businesses and Individuals

The proposed reforms mark a positive shift toward a more modern and internationally aligned tax system. Businesses and individuals should assess how these changes could impact their tax liabilities and long-term financial planning.

How Doviandi Can Help

Doviandi specializes in corporate tax planning, Cyprus company formation, and business relocation services. Our team can assist with:

- Impact Assessments to evaluate how the proposed tax changes may affect your business.

- Strategic Tax Planning to optimize corporate structures under the new regulations.

- Personal Tax Advisory for individuals seeking to benefit from Cyprus’s tax advantages.

Stay ahead of the changes and ensure your business remains tax-efficient. Contact Doviandi today for a tailored consultation.